What is Construction Mortgage?

Construction Mortgage as the name goes is a type of mortgage that allows you to finance the construction of your home. The concept is that it allows you to finance the purchase of a home that may not even exist yet – whether you are designing it or purchasing a pre-build in a development project.

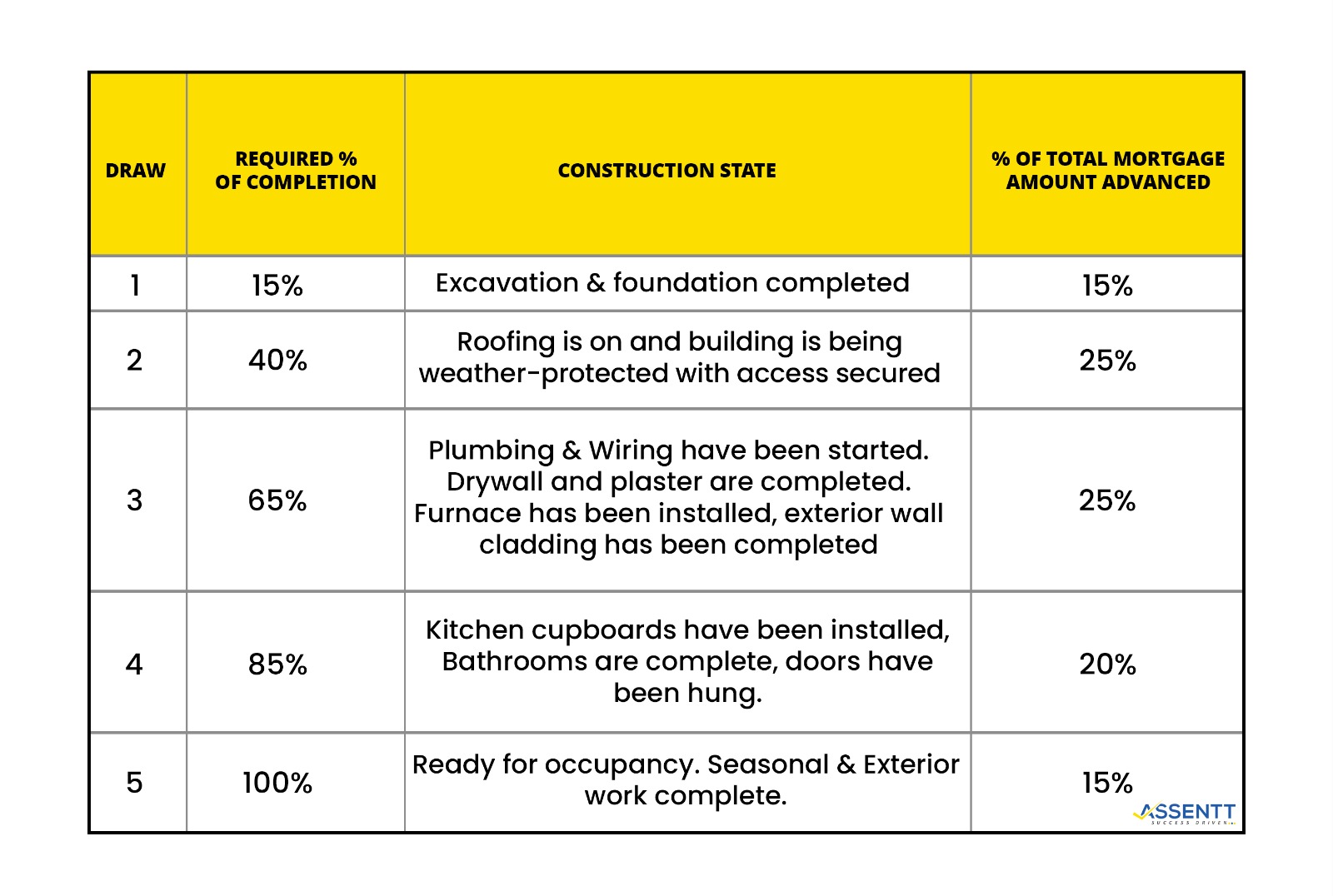

Construction mortgage is also commonly referred as builder’s mortgage in Canada. Unlike traditional mortgage where funds are paid in a single payment to the seller on the closing day, here you are paid out in smaller increments (referred as draw) as each phase of construction is completed. That is, as the construction keeps proceeding, the funds keep getting released.

This kind of mortgage is most common with people who already have a plot of land and looking to build on it their dream house.

How Construction Mortgage Works :

If you are planning to build your home from scratch on an already purchased plot or planning to buy one then Construction Mortgage is the ultimate financing solution. If you already have a plot of land then first advance is available as equity take-out and if you haven’t yet bought a piece of land then it assists you with the purchase of a vacant lot.

Construction mortgage like most loans requires a down payment. They come in fixed or variable-rate options with the possibility (in some cases) of converting to a traditional mortgage once construction is complete and certificate of occupancy is received.

Construction Mortgage requires inspections each step before the next draw is approved. The borrower owes the inspection costs which may be deductible from each draw. Till the construction isn’t complete, some lenders may require you to pay interest on the amount borrowed and once construction is complete, you are required to make payments of both principal and interest.

Draw Schedules for a Construction Mortgage :